全東信の破綻から考える ― ビジネスモデルと「Exit設計」

全東信の破綻から考える ― ビジネスモデルと「Exit設計」

全東信の破綻について、「粉飾決算」や「1,000億円を超える負債」が大きく報じられています。

しかし、この事件を理解するには、まずビジネスモデルを理解する必要があります。

全東信はクレジットカード決済代行会社と紹介されますが、本質はそれだけではありません。

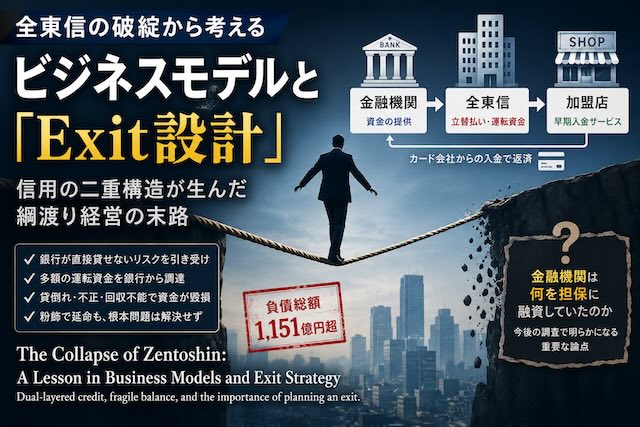

加盟店は通常、カード会社から売上代金を受け取るまで数週間待たなければなりません。全東信は、その入金を待たずに加盟店へ先に資金を支払うサービスを提供していました。

つまり、カード会社から後日入金される売掛債権をもとに、加盟店へ早期に資金を供給するビジネスです。実質的には、短期金融やファクタリングに近い仕組みといえます。

このモデルでは、全東信は多額の運転資金を必要とします。そのため、金融機関から資金を調達し、カード会社から入金された資金で返済するというサイクルを繰り返していました。

ここで興味深い点があります。

全東信の取引先には、銀行から十分な融資を受けにくい加盟店も多く含まれていました。一方で、その全東信自身は60社を超える金融機関から1,000億円を超える資金を調達していました。

つまり、

銀行 → 全東信 → 加盟店

という「信用の二重構造」が形成されていたことになります。

もちろん、このモデル自体が間違っているわけではありません。

カード会社からの入金が確実であり、適切な与信管理と十分な自己資本があれば成立するビジネスです。

しかし、この構造には本質的な難しさがあります。

銀行が直接融資しにくいリスクを全東信が引き受け、その全東信を銀行が支える構造だからです。

一度、加盟店の貸倒れや不正利用、回収不能などによって資金の流れが崩れれば、全東信は銀行からの追加資金に依存せざるを得なくなります。そして、その実態を粉飾で隠せば、一時的に時間を買うことはできても、問題そのものは解決しません。

今回の事件で、私が最も関心を持っている論点があります。

金融機関は、何を担保に1,000億円を超える資金を融資していたのでしょうか。

カード会社からの入金債権を裏付けとしていたのか。

それとも、全東信という会社自体の信用力を前提としていたのか。

あるいは、その両方だったのか。

もしカード会社からの入金債権が十分に裏付けられていたのであれば、ここまで大きな損失はなぜ発生したのでしょうか。

一方で、実態以上に信用供与が行われていたのであれば、金融機関の与信管理についても検証が必要になります。

この点は、破産管財人や今後の調査で明らかになっていく重要な論点だと思います。

経営者に本当に求められるのは、「どう成長するか」だけではありません。

どこで損失を認めるのか。

どこで事業を縮小するのか。

どこでスポンサーを探すのか。

つまり、「Exit」を設計することです。

粉飾決算は会計の問題として語られがちですが、本質はそうではありません。

Exitを設計できなかった経営の問題です。

成長戦略だけでなく、撤退戦略も経営戦略の一部です。

全東信の破綻は、そのことを改めて示した事例ではないでしょうか。

The Collapse of Zentoshin: A Lesson in Business Models and Exit Strategy

The collapse of Zentoshin has attracted attention because of its accounting fraud and liabilities exceeding ¥100 billion.

However, to understand what really happened, we must first understand its business model.

Zentoshin is often described as a credit card payment processor. In reality, its business was much closer to a short-term finance company.

When a customer pays by credit card, merchants normally wait several weeks before receiving funds from the card issuer. Zentoshin advanced those funds before settlement.

In other words, it converted future receivables into immediate cash. Economically, the model resembled factoring or short-term receivables financing.

Such a business requires substantial working capital. Zentoshin borrowed funds from financial institutions, advanced cash to merchants, and repaid those borrowings when the card issuers settled the receivables.

This created an interesting structure.

Many of Zentoshin’s merchant clients had limited access to bank financing. Yet Zentoshin itself obtained more than ¥100 billion in funding from over sixty financial institutions.

The structure therefore became:

Banks → Zentoshin → Merchants

The model itself is not inherently flawed.

If receivables are genuine, collections are reliable, credit risk is well managed, and capital is sufficient, it can operate successfully.

The challenge lies elsewhere.

Zentoshin assumed risks that banks were reluctant to take directly, while relying on those same banks to finance its operations.

Once merchant defaults, fraud, chargebacks, or collection problems disrupted the cash flow, the company inevitably became more dependent on external funding. If accounting manipulation was then used to conceal the deterioration, time might have been bought temporarily, but the underlying problem remained.

The question that interests me most is this:

What exactly were the banks lending against?

Were they primarily financing receivables from the card companies?

Or were they relying on Zentoshin’s own corporate credit?

Or was it a combination of both?

If the receivables were genuine and sufficiently secured, why did losses become so large?

If the lending relied more heavily on the company’s reported financial condition than its actual receivables, then the effectiveness of the banks’ credit assessment also deserves careful examination.

The answers to these questions will likely emerge through the bankruptcy proceedings.

For management, the most important challenge is not simply how to grow.

It is when to recognize losses.

When to reduce the business.

When to seek new investors.

In other words, how to design an exit.

Accounting fraud is often viewed as an accounting issue.

In reality, it is more often a failure of management to make difficult strategic decisions before options disappear.

Growth strategy matters.

Exit strategy matters just as much.

The collapse of Zentoshin reminds us that sustainable management requires both.

大原達朗が行うBBT大学での講座93%が満足と回答したファイナンスドリブンキャンプ

本講座では、短期間でCFO(最高財務責任者)への第1歩を踏み出すことを目指します。大量の決算書に触れ、大量にアウトプットし、大量のフィードバックを通してファイナンスという武器を手に入れられます。ブログでは話せない「ライブ講義」も充実しています。まずは無料説明会を受講してみて下さい。

本誌について

本誌は、M&Aを売り手、買い手、アドバイザーが三方良し、となるのが当たり前の世界の実現を目指しています。そのためには当事者が正しい情報を得て、安心して相談のできる場が必要です。その実現に向けて本誌は、日本M&Aアドバイザー協会で、以下のサービスやセミナーを提供しております。

| M&A仲介・アドバイザーを事業としたい方・既にされている方へ | |||

|---|---|---|---|

| セミナー・サービス名 | 詳細 | 金額 | 時間 |

| 誰にでもわかるM&A入門セミナー | ・会場開催の詳細とお申込み ・オンライン講座の視聴 |

無料 | 2時間 |

| M&A実務スキル養成講座 | ・会場開催の詳細とお申込み ・オンライン開催の詳細とお申込み ・M&A実務スキルの詳細 |

198,000円 | 2日間 |

| JMAA認定M&Aアドイザー資格取得およびJMAA会員に入会 | ・資格詳細とお申し込み | 入会金33,000円 月会費11,000円(1年分一括払) | - |

| 案件サポート制度 | JMAA会員が初めてM&Aアドバイザリー業務に取り組む場合、あるいはすでに何度かアドバイザリー業務に経験があっても、難易度が高い案件の場合のための、JMAA協会が会員に伴走して案件成約に向けて協力する制度です。 お申し込みは当協会ご入会後にお知らせします。 | JMAA正会員の関与する対象案件の成功報酬の50% | - |

| 買収を検討されている企業団体様へ | |||

| セミナー・サービス名 | 詳細 | 金額 | 時間 |

| 誰にでもわかるM&A入門セミナー | ・会場開催の詳細とお申込み ・オンライン講座の視聴 |

無料 | 2時間 |

| M&A実務スキル養成講座 | ・会場開催の詳細とお申込み ・オンライン開催の詳細とお申込み ・M&A実務スキルの詳細 |

198,000円 | 2日間 |

| 買い手様向けセカンドオピニオンサービス | ・M&Aセカンドオピニオンサービスの詳細 | 33,000円 追加相談サービス 33,000円/1時間 | 1時間〜 |

| 売却を検討されている企業団体様へ | |||

| セミナー・サービス名 | 詳細 | 金額 | 時間 |

| 誰にでもわかるM&A入門セミナー | ・会場開催の詳細とお申込み ・オンライン講座の視聴 |

無料 | 2時間 |

| M&A実務スキル養成講座 | ・会場開催の詳細とお申込み ・オンライン開催の詳細とお申込み ・M&A実務スキルの詳細 |

198,000円 | 2日間 |

| 売り手様向けセカンドオピニオンサービス | ・M&Aセカンドオピニオンサービスの詳細 | 33,000円 | 1時間〜 |

M&A実務を体系的に学びたい方は、M&A実務スキル養成講座

メルマガ登録はこちら

ファイナンスドリブンキャンプ

生成AIキャンプ

大原達朗の経営リテラシー-自ら考え、行動しよう-